|

Taxes and Taxation

Reference:

Valova A.A.

Digital currencies of central banks and cryptocurrencies. Role in compliance with tax legislation.

// Taxes and Taxation.

2023. ą 3.

P. 10-20.

DOI: 10.7256/2454-065X.2023.3.40712 EDN: ZAWJGI URL: https://en.nbpublish.com/library_read_article.php?id=40712

Digital currencies of central banks and cryptocurrencies. Role in compliance with tax legislation.

Valova Anna Aleksandrovna

ORCID: 0000-0003-2296-8824

Postgraduate student, Financial University

125057, Russia, Moscow, Leningradskii Prospekt, 49/2

|

valovs@yandex.ru

|

|

|

Other publications by this author

|

|

|

DOI: 10.7256/2454-065X.2023.3.40712

EDN: ZAWJGI

Received:

06-05-2023

Published:

13-05-2023

Abstract:

The use of private digital assets based on distributed ledger technology and cryptography methods is increasing every year. The opportunities provided by crypto assets due to their special characteristics can be used when issuing digital assets controlled by the state. The subject of this article is the study of digital currencies of central banks (CBDC), the digital ruble, consideration of their differences from cryptocurrencies and the opportunities provided by them to strengthen tax control in the field of compliance with tax legislation by subjects of economic relations. The research was carried out using universal (analysis, generalization) and special legal methods of cognition (comparative legal, historical legal). The novelty of the study consists in updating approaches to identifying the essence of digital currencies of central banks, including the digital ruble and the possibility of their influence on compliance with tax legislation. As a result of the study, the author concluded that the need to introduce digital currencies of central banks is now under active study by the central banks of a large number of states. The advantages for users of these assets will be speed, availability of assets even in regions that are difficult to access for banking services and security from the state. For regulators, the introduction of these assets will reduce interest in cryptocurrencies, transactions with which are often made for illegal purposes, as well as give additional incentives in the fight against tax evasion.

Keywords:

digital currencies, cryptocurrencies, digital assets, digital ruble, tax evasion, fiat money, digital technologies, blockchain, Central Bank of Russia, distributed ledger

This article is automatically translated.

You can find original text of the article here.

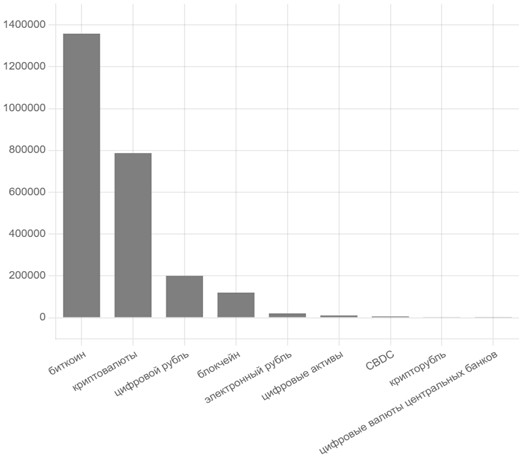

IntroductionThe growing use of digital technologies around the world has contributed to the emergence of new types of digital assets that can compete with traditional means of payment and financial instruments. Cryptocurrencies, digital financial assets, smart contracts are widely used by subjects of economic relations that take advantage of these types of assets. Speed, low transaction costs, anonymity, the absence of intermediaries in the form of banks, accessibility to the general public and the possibility of cross-border transactions with digital assets increase the popularity of these tools. Only in April 2023 the interest of Russian-speaking users of the search engine “Yandex” in the field of cryptocurrencies amounted to about 800 thousand requests per month, more than 1 million people were interested in information about the most popular cryptocurrency - bitcoin. Search engine query statistics “Yandex” in the field of digital assets in April 2023 is shown in Figure 1.

Fig.1 Search engine query statistics “Yandex” in relation to digital assets in April 2023Source: compiled by the author on the basis of the Yandex service to assess the user interest of wordstat. yandex.ru https://wordstat.yandex.ru/ The interest in digital assets based on distributed ledger technology and cryptography methods is closely related to the general trend of decreasing cash payments in retail transactions in various states. Against the background of this trend, new digital assets used as means of payment are gaining their niche and compete not only with cash, but also affect the use of cash by subjects in non-cash form. Thus, according to forecasts of Deutschebank specialists, by 2030 the rapid growth of digital payments, including convenient mobile payments, may lead to a complete rejection of the use of bank cards [1].Although the impact of the most popular types of crypto assets - cryptocurrencies on global payment systems is currently small [2], given the constant improvement of these assets, the emergence of new types, in particular, stable coins (stablecoins), not subject to such high volatility as unsecured cryptocurrencies, some experts believe that cryptocurrencies have potential for a global change in the payment system and even the role of central banks in them [3]. It is no coincidence that central banks of different countries were among the first at the level of state regulators to pay attention to the problems associated with the growth of crypto assets and in particular cryptocurrencies [4]. Currently, there are concerns that stablecoins, including cryptocurrencies issued by corporations controlling social networks (Facebook, Telegram) may threaten the stability of the global economy, so regulators prevent their release [5]. The Central Bank of Russia is no less critical, considering cryptocurrencies as a whole as a threat to the financial stability of the country due to the risks created of undermining the sovereignty of the national currency when using cryptocurrencies as means of payment [6]. Nevertheless, in the conditions of general digitalization, such opportunities of cryptocurrencies as accessibility to the general public without the need to open bank accounts, cheapness and speed of transactions, the impossibility of falsifying payments due to functioning on the blockchain can be useful and taken as a basis for the transformation of traditional forms of means of payment. Currently, the central banks of various states are conducting research to study the need to add a digital form to the already existing two forms of national currencies (cash and non-cash), which would combine the best properties of crypto assets, while remaining controlled by the state. The purpose of this article is to study new types of digital assets, in particular digital currencies of central banks (CBDC) in comparison with cryptocurrencies and the role of the former in strengthening state control in the fight against tax evasion. Both central banks of developed countries and regulators in developing countries are currently studying the need to introduce these types of assets and testing pilot projects. The author explores the prospects and advantages of introducing these types of digital assets, including the digital ruble, their difference from cryptocurrencies and the impact on compliance with tax legislation by subjects of economic relations. The issues of the introduction of digital currencies of central banks of foreign states, their relationship with cryptocurrencies, the emergence of the digital ruble and the impact on the banking system were partially considered in the works of A.A. Sitnik, N.K. Norets, D.M. Sakharov, O.V. Vershinina, D.A. Kochergin, while the introduction of digital currencies of central banks into the economy in the context of compliance tax legislation has not been studied in the domestic literature before. To achieve the purpose of the study, the author of the article set tasks: to identify the nature of digital currencies of central banks, to compare with cryptocurrencies, to identify possible advantages from the introduction of digital currencies of central banks, to assume their impact on the implementation of state control, including tax control in the field of combating tax evasion and increasing tax collection. Material and methods The research used analytical materials of the Central Bank of the Russian Federation, the Financial Stability Board (FSB), the Organization for Economic Cooperation and Development (OEDC), the work of scientists and specialists on relevant topics. The processing of the obtained data was carried out using universal (analysis, generalization) and special-legal (comparative-legal, historical-legal) methods of cognition.

Central Bank Digital Currencies and Crypto AssetsDigital currencies of central banks (CVCB) are a new digital asset, the interest in which is currently at the peak of popularity on the part of central banks of various states. According to analysts, in May 2020, 35 states considered the issues of the Central Bank. Over the past four years, the number of central banks actively involved in the issue of central securities has increased significantly. As of 2021, more than 80 states with a share of global GDP of more than 90% were at various stages of studying or implementing digital currencies of central banks in their jurisdiction [7]. At the same time, according to the analytical Internet resource “CBDC Tracker”, as of April 2023, more than 130 states were already dealing with the issues of the Central Bank [8]. The main statistical facts about the Central Bank as of 2023 are shown in Figure 2.

Fig.2 Data on the introduction of CVCS in the world as of April 2023Source: compiled by the author based on [8]

Technically, various models of the introduction of CVCB are possible. They can be based both on distributed registry technology (blockchain) and on a centralized model. They can be retail (for public use), wholesale (for use by financial institutions) or hybrid models combining the properties of the first two. In 2020, the Central Bank of Russia published a report for public consultations on the digital ruble, in which possible models of the introduction of the digital currency by different states were presented [9]. These models are shown in Table 1. Table 1 Countries' Choice of the central bank's Digital Currency Model | A countryWholesale or retail | Tokens or accounts | Distributed registry or centralized | Project status | China | | | retail | tokens | distributed | piloting |

| South Korea | retail | tokens | discussion | piloting | | USA | both | tokens | distributed | research | | Great Britain | retail | discussed | discussed | research | | Switzerland | wholesale | discussed | discussed |

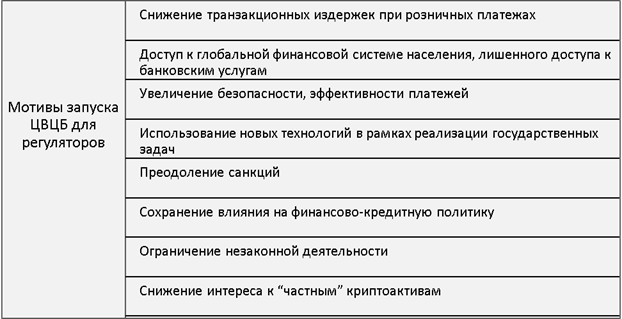

research | | Eurozone | retail | accounts | discussed | research | Source: compiled by the author on the basis of [9]. The attention of states to centralised and controlled digital securities, but at the same time combining the advantages of new technologies, is due to various reasons. The main motives that guide the central banks of various states when considering the need to issue securities are shown in Figure 3.

Fig.3 Motives for launching digital currencies of central banks by regulators Source: compiled by the author

The last few reasons given in Figure 3 are closely related to the increasing spread of cryptocurrencies, transactions with which, due to their special characteristics, are difficult to control by government agencies. Often, digital currencies of central banks are compared with cryptocurrencies, the digital ruble is called a “crypto ruble”, but despite the apparent similarity between these digital assets, the differences between them are fundamental. Digital currencies of central banks are primarily a new digital form of money, which should be circulated along with cash in cash and non-cash forms. In the report of the Central Bank of Russia on the digital ruble, the bank indicated its intention to study the needs and prospects of issuing a digital ruble in the context of the need for the monetary circulation system to meet the changing needs of economic entities [9], in 2021 the concept of the digital ruble was released [10]. In these documents, the Central Bank of the Russian Federation confirmed that the digital ruble should combine the best properties of cash and non-cash money, should be constantly available for settlement, including providing offline payments. It should be noted that regardless of the chosen variant of the Central Securities Exchange model, these currencies existing in digital form will, on the one hand, differ significantly from cryptocurrencies, but, on the other hand, they are able to compete with them or at least reduce the interest of transaction participants in settlement transactions using cryptocurrencies, incorporating the best features crypto assets. According to N.K. Norets, who conducted a study of the digital ruble and cryptocurrencies, since these assets have different legal nature, comparing these two assets is not entirely appropriate [11]. Digital currencies of central banks, including the digital ruble, are indeed full-fledged means of payment, one of the forms of fiat money, while cryptocurrencies do not possess all the properties of money. D.A. Sakharov takes a similar position, pointing out that cryptocurrencies cannot be considered money, since the function of a measure of value and a means of accumulation is not performed, offering to call cryptocurrencies more precisely crypto assets. At the same time, the latter are designed not to counteract, but to complement cryptocurrencies [12], with which, however, A.A. Sitnik does not agree, noting that the introduction of digital currencies of central banks into circulation will hinder the process of “privatization of monetary circulation” [13]. The comparative characteristics of the digital currencies of central banks and cryptocurrencies can be presented in the form of a table. Table 2 Comparison of digital currencies of central banks and cryptocurrencies

| Digital currencies of central banks | Cryptocurrencies | Controlled by | | | by the issuer (central bank) | decentralized, not controlled by a single center | | Issue | by the issuer's decision | not limited/limited in the case of bitcoin | | Provision | state | missing/partially present by stablecoins | | Is it money | yes, one of the forms | no | | Cost of maintenance | low | low | | The level of trust | high |

can change quickly | | The level of anonymity of transactions | low | high | | The level of volatility | low | high | Source: compiled by the author on the basis of [11]. Digital currencies of central banks and tax controlThe low level of anonymity of digital currencies of central banks is a significant advantage for the state, suggesting the possibility of enhanced state control over transactions. The so-called “programmability” of digital currencies, the technical characteristics of which allow rationing expenses or making them targeted, is also associated with this possibility. In particular, it will be possible to provide subsidies to individual economic entities in the form of “digital rubles”, the spending of each of which can be traced to the provided purposes and, accordingly, it will be possible to assess the effect of the provided support measures. In addition to significant advantages in controlling the expenditure of budgetary funds, of course, transparency of information when using central securities in transactions that resulted in taxable income will simplify the possibilities of tax administration of transactions that could previously be withdrawn from taxation, including through the use of cash payments or cryptocurrencies. The peculiarity of digital currencies of central banks is the presence of a “digital footprint” or digital memory of previous owners and their operations, which makes it possible to detect dubious or illegal transactions in which digital currencies were used. It is a well-known fact that the use of digital payments instead of cash occupies a central place in the policy of combating the laundering of proceeds from crime. A number of states are constantly encouraging the use of electronic payments, introducing both total restrictions on cash payments and providing various, including tax benefits to participants of electronic payments. For example, L. Scarsella, in his study on the prospects of tax policy in connection with the introduction of the Central Bank, notes that in Colombia, Mexico, from a certain period, tax deductions in the form of certain expenses can be provided only when making transactions using bank cards or electronic transfers. In Italy, starting from 2020, expenses incurred using tracked means of payment can be taken into account in the same way when calculating personal income tax [14]. Thus, the adoption of legislation on digital currencies of central banks would allow states to pursue a tougher policy against money laundering and tax evasion by reducing the anonymity of transactions. In addition, the growth of tax revenues to the budget could be ensured not only by strengthening tax control with the help of CBDC, but also due to the possible automation of the processes of calculating and paying taxes. This is possible when using programmable “smart contracts”, when already at the time of receiving income using digital currencies, the tax would immediately be calculated automatically to the budget. The above-mentioned opportunities are certainly attractive to state regulators, but from the point of view of business entities, the downside is important, namely the issues of anonymity and confidentiality of transactions. In the case of cryptocurrencies, the issue of anonymity is often crucial when choosing this instrument by the participants of transactions. In a fairly large number of cases, cryptocurrencies, due to their properties, can be used in illegal activities or participate in tax evasion schemes due to the inability to control income generation using traditional tools in the absence of special rules in tax legislation. Accordingly, unscrupulous business entities, if they can choose between cryptocurrency and cash or the digital currency of the central bank, in particular, the digital ruble, will not make it in favor of the latter.

On the other hand, the opportunities for abuse with the introduction of CVCS will be reduced. According to some authors, if less anonymity is provided when using digital currencies of central banks than when using cash payments, the introduction of a new form of currency will reduce tax evasion. However, if the use of the Central Bank is designed with a high degree of anonymity, then its implementation will not only allow unscrupulous persons to use the tool, but also reduce the return on income from bona fide taxpayers [15]. It seems that for bona fide business entities, the issue of confidentiality when making payments will also be important from the point of view of non-interference in personal life, and the ability to use currency in a new digital form without unnecessarily collecting information about users may be of great importance here. A number of researchers, when considering the scenario of the complete replacement of digital securities with other forms of fiat money, make assumptions about the emergence of a “dystopia” due to the fact that digital securities are an ideal tool for total control by the state, since the integration of digital securities into the economy will allow the state not only to control, but also to limit the spending and movement of their users [16]. We believe that this scenario is unlikely, at least because none of the central banks investigating the Central Securities Market has stated the need to completely replace existing forms of money with a new digital form. A more likely scenario is the introduction of central securities as an addition to the already existing forms of fiat currencies, allowing owners to take advantage of digital technologies provided by the state. At the same time, of course, the issues of balancing the interests of regulators and bona fide users in the field of information confidentiality are very important and are being considered at the state level. In China, for example, this issue is proposed to be solved through the concept of “controlled anonymity”, when information about large transactions is less anonymous than data on small retail payments. It will be possible to hide the data of users of the digital yuan from counterparties, but at the same time they can be accessed by law enforcement agencies if necessary, however, as D.A. Kochergin correctly notes, no one can guarantee how this will actually happen [17]. We believe that it would be reasonable to make transactions with digital currencies of central banks, including the digital ruble, with the same degree of anonymity as when making non-cash settlements with the mediation of banks, i.e. in accordance with the rules to which users are already accustomed. Conclusion The need to introduce digital currencies of central banks is currently under active study by regulators of various states. The global interest on the part of central banks in this form of payments is caused by the development of digital technologies that allow solving a number of government tasks with the help of new tools, as well as adapting to the realities of modern life. The advantages of introducing digital currencies of central banks for users will be the opportunities provided by these assets, combining the best features of crypto assets and traditional means of payment. Low transaction costs during settlements, speed, the possibility of “offline” settlements even in remote regions, security and security on the part of the state may interest conscientious business entities to use this form of funds in their daily operations. For states, the introduction of digital currencies by central banks will help maintain the stability of the financial system during the period of increasing use of crypto assets and reduce interest in cryptocurrencies, improve state control over transactions, since each transaction will be registered in a database accessible to various government agencies, if necessary. Accordingly, the use of central securities may give regulators additional incentives in the fight against tax evasion and illegal transactions. A further tendency to reduce the use of cash in transactions as the least controlled option for making settlements from the point of view of tax administration and the embedding of a new form of cash in the form of digital currencies of central banks into calculations may simplify control over compliance with tax legislation by tax authorities. In addition, if necessary, it is possible to program transactions with digital securities based on blockchain to automatically pay tax upon instant receipt of income by the transaction participant, which can also increase tax collection. When designing the rules for the functioning of digital currencies of central banks, it is important to find an optimal balance between the interests of the state and taxpayers, related to the permissible degree of confidentiality of transactions for bona fide taxpayers, as well as the protection of information, while being able to detect and prevent violations of legislation and exercise state control.

References

1. Deutsche Bank Research. The Future of Payments: Part II. Moving to Digital Wallets and the Extinction of Plastic Cards. (2020). URL:// https://blog.alegra.com/wp-content/uploads/2020/04/The_Future_of_Payments_-_Part_II__Moving_to_Digita.pdf

2. Financial Stability Board. Assessment of Risks to Financial Stability from Crypto-assets. (2022). URL: https://www.fsb.org/2022/02/assessment-of-risks-to-financial-stability-from-crypto-assets/

3. Deutsche Bank Research. The Future of Payments:Part III. Digital Currencies: the Ultimate Hard Power Tool. (2021). URL:https://cashessentials.org/app/uploads/2021/04/The_Future_of_Payments_-_Part_III__Digital_Currenc.pdf

4. OECD. Taxing Virtual Currencies: An Overview Of Tax Treatments And Emerging Tax Policy Issues, OECD. (2020). URL: https://www.oecd.org/tax/tax-policy/taxing-virtual-currencies-an-overview-of-tax-treatments-and-emerging-tax-policy-issues.pdf

5. Scott, A. Burns (2019). If Libra Threatens Central Bank Power, that’s Great. URL: https://www.aier.org/article/if-libra-threatens-central-bank-power-thats-great/

6. Bank of Russia. Cryptocurrencies: trends, risks, measures. Report for public consultation. (2022). URL: https://cbr.ru/Content/Document/File/132241/Consultation_Paper_20012022.pdf

7. Aran, Ali. (2021). How Central Banks Think About Digital Currency. URL: https://www.visualcapitalist.com/how-central-banks-think-about-digital-currency/

8. Open analytical Internet resource CBDC Tracker. (2023). URL: https://cbdctracker.org/cbdc-tracker-whitepaper.pdf

9. Bank of Russia. Digital ruble. Report for public consultation. (2020). URL: http://cbr.ru/analytics/d_ok/dig_ruble/

10. Bank of Russia. The concept of the digital ruble. (2021). URL: https://cbr.ru/Content/Document/File/120075/concept08042021.pdf

11. Norets, N.K. (2021). Is the digital ruble a cryptocurrency: a comparative analysis // Scientific Bulletin: Finance, banks, investments, 3, 90-96.

12. Sakharov, D.M. (2021). Central Bank Digital Currencies: Key Features and Impact on the Financial System. Finance: theory and practice. 25(5),133-149. URL: http://elib.fa.ru/art2021/bv2046.pdf/download/bv2046.pdf

13. Sitnik, A.A. (2020). Digital currencies of central banks. Bulletin of Kutafin University, 9. URL: https://vestnik.msal.ru/jour/article/view/1227

14. Scarcella, L. (2020). Adopting a Central Banking Digital Currency: A Tax Policy Perspective. URL: https://www.afronomicslaw.org/2020/12/02/adopting-a-central-banking-digital-currency-a-tax-policy-perspective

15. Wang, Z. (2020). Tax Compliance, Payment Choice, and Central Bank Digital Currency. URL: https://ssrn.com/abstract=3755573

16. CBDC as a means of total control (2022). URL: https://media.sigen.pro/allarticles/9110?ysclid=lhdfnjkjsk964291625

17. Kochergin, D. A. (2022). Digital currencies of central banks: the experience of introducing the digital yuan and the development of the concept of the digital ruble // Russian Journal of Economics and Law. 16, 1. 51–78. URL: https://cyberlininka.ru/article/n/tsifrovye-valyuty-tsentralnyh-bankov-opyt-vnedreniya-tsifrovogo-yuanya-i-razvitie-kontseptsii-tsifrovogo-rublya?ysclid=lhisozgtoo18836717

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study. It seems that the current name needs to be adjusted, because based on it, the article should disclose issues related to the role of digital currencies of central banks and cryptocurrencies in compliance with tax legislation. Can digital currencies or cryptocurrencies play a role in tax compliance? If so, this aspect is not disclosed in the text of the reviewed article. Moreover, the name contains two sentences, which is not accepted when forming headings (also, the dot in the name is also not put). At the same time, if we clarify the name of the option, the content of which will focus on studying the parameters of the development of the concept of the digital ruble and its implementation, then there will be no contradictions. Research methodology. The research is based on the use of traditional scientific methods (data analysis and synthesis), which allowed the author to draw a number of conclusions in the context of the stated topic. This article also positively characterizes the quality of the use of graphical tools (building tables and graphs), which made it possible to visually demonstrate the results of the study. The relevance of the study of issues related to the development of the concept of the introduction of digital currencies is of interest both to the scientific community and to officials of state authorities of the Russian Federation, the Central Bank of the Russian Federation. The scientific novelty is contained in the material submitted for review. It is related to the results of the analysis of query statistics in the Yandex search engine regarding digital assets in April 2023, as well as certain motives for the launch of digital currencies by central banks from regulators. These results can be used in real practical activities of the Ministry of Finance of the Russian Federation, the Ministry of Economic Development of the Russian Federation, the Ministry of Finance of the Russian Federation, the Bank of Russia, including in the formation of the infrastructure for the functioning of the digital ruble. Style, structure, content. The style of presentation is scientific. The structure of the article is built logically, allows you to competently immerse yourself in the content of the issues under consideration (if we assume that they are in line with various aspects of the introduction of the digital ruble). The content of the article focuses on the study of the prerequisites for the launch of digital currencies of central banks by regulators, which can be used in the activities of the Bank of Russia. The bibliographic list consists of 17 titles. At the same time, the author has insufficiently studied the scientific literature on the issues under consideration. At the same time, quite a lot of scientific publications have been published in both domestic and foreign publications in the last few years. Appeal to opponents. Despite the existence of a generated list of sources, the author does not carry out their critical analysis and discussion of the results obtained. When making improvements, attention should be paid to solving this problem. Conclusions, the interest of the readership. Taking into account all the above, the article is executed at a good level, but in order to ensure a high level it requires an adjustment of the title, a review of sources and a strengthening of the quality of recommendations (including in connection with the identified problems and motives). The article is of interest to a wide range of readers, including practitioners. At the same time, the revision of the article will significantly expand it.

|

Eng

Eng